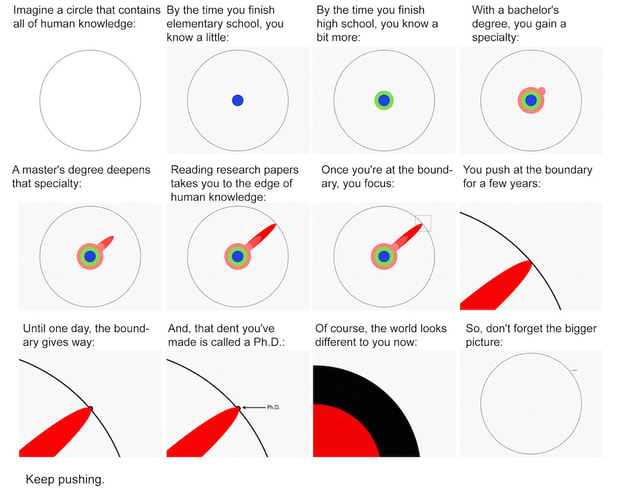

I’ve loved this graphic ever since I saw it 5+ years ago. Getting close to the edge of human knowledge is exciting. Expanding it and leaving a little dent on the world is even better. Whilst this sentiment might be well understood by academia, there are many parallels in the business world that aren’t adequately appreciated.

The Best Way to Predict the Future is to Invent It In the 1970s, Alan Kay, best known for his work on object-oriented programming and graphical user interfaces (GUIs), famously said that the best way to predict the future is to invent it. We may not all be pioneering engineers or physicists working on a unified theory, but there is still ample opportunity to have an impact. Moving over to the domain of startups, founders are often told they need to have a “unique insight” when it comes to building a business. This advice can be frustrating because it’s vague and not directly actionable. The image above is a good way to visualise what it means to have unique insight. So, how does one get there? Unsurprisingly, Paul Graham’s advice is well articulated. “Once you've found something you're excessively interested in, the next step is to learn enough about it to get you to one of the frontiers of knowledge. Knowledge expands fractally, and from a distance its edges look smooth, but once you learn enough to get close to one, they turn out to be full of gaps.” As he explains, this has four steps: “Choose a field, learn enough to get to the frontier, notice gaps, explore promising ones. This is how practically everyone who's done great work has done it, from painters to physicists.” I’d add two more things:

Should You Specialise Early? This is something I consistently debate with friends. The concept of a “T-shaped person”, popularised by David Epstein’s book Range, is apt. A T-shaped person is someone who has deep knowledge and skills in one area (the vertical bar of the T) and a broad base of knowledge and skills in other areas (the horizontal bar of the T). In other words, a T-shaped person is a generalist with expertise in a specific field. Whilst there are benefits to being T-shaped (particularly in business), I’d argue that not enough young people (myself included), spend sufficient time thinking about which frontiers they want to approach. The reasoning is simple. Many people approach the edge naturally in their careers. If you spend 30 years doing the same thing, you’re likely within striking distance. This is great, but the quicker you can get there, the more time you have to do meaningful work. Two extreme examples of this would be Stripe and Brex. The Collison brothers were 19 and 21 when they founded Stripe, and the Brex founders were both 22. Both companies were born out of personal frustration, followed by a process of rapid learning in pursuit of the edge. Most 20-somethings aren’t thinking about payment processing or expense management. But if you’re purposeful about expediting your journey to the edge, the more at-bats you get. If You Can’t Invent the Future, Try and Invest In It If inventing the future isn’t your cup of tea, investing behind it is not a bad option. People sometimes describe this as the job of Venture Capital – investing in the ambitious founders who live 5 years ahead of the rest. Regardless of whether you plan to invest personally or professionally, being close to the edge allows you to invest in trends ahead of them becoming mainstream. Learning from founders living in the future has been the best part of my time at AirTree. If you’re one of these people tinkering on the edge, I’d love to chat. In 1960, J.C.R. Licklider, a man widely considered to be one of the fathers of modern computing, famously authored the paper Man-Computer Symbiosis. In it, he painted an illustrative picture of the way humans and computers would interact with each other. At the time, many considered it to be a grand illusion. More than 60 years later, LLMs have exploded onto the scene and many of his visions don’t seem too far-fetched. In this article, I’ll share some very rough hypotheses on what this may look like.  The Fig Tree Licklider provides an eloquent analogy: “The fig tree is pollinated only by the insect Blastophaga grossorun. The larva of the insect lives in the ovary of the fig tree, and there it gets its food. The tree and the insect are thus heavily interdependent: the tree cannot reproduce without the insect; the insect cannot eat without the tree; together, they constitute not only a viable but a productive and thriving partnership. This cooperative 'living together in intimate association, or even close union, of two dissimilar organisms' is called symbiosis.” His hope was that humans and computers would be coupled together very tightly, with the resulting partnership thinking “in a way no human brain has ever thought and processing data in a way not approached by the information-handling machines we know today”. Where Are We Now? Anyone who’s experienced the magic of LLMs will agree that we’ve levelled up in mankind’s inevitable march towards symbiosis. But what might this symbiosis look like in 10 years? Here are two somewhat opposed concepts that I’ve been thinking about: extreme delegation to AI agents, and hyper-personalisation. [1] Extreme Delegation to AI Agents (sans Decision Making) Imagine a world where we interact with software tools and each other via our own AI agents. If I need to create a presentation with my team, our AI agents collaborate by going into Gmail and Notion to understand all relevant context, and then spin something up in Canva. Then they report back to us with a list of questions, find us a time to meet, create an agenda, and we respond to their questions to drive the next iteration of the presentation. Or, if we’re a lean startup developing a new feature, our AI agents across engineering, marketing and operations come together to build a roadmap. Along the way, they ask us questions and use this feedback until they present a holistic plan. Then they go and autonomously build the feature. This might sound far-fetched, but with tools like AutoGPT and Rewind, AI agents will be able to understand all the necessary context and execute tasks by breaking them into sub-tasks. Furthermore, these agents will be able to collaborate, mostly without a human in the loop. This brings to mind three implications:

Choose Your Own Adventure If that all sounds pretty grim, let me paint another picture. A popular narrative today is that with AI, we will be able to create anything we want – whether it be a novel, a TV show, or even software. I find this logic fascinating because whilst humans inherently have the desire to be creative, we are also inherently lazy. We might experiment every now and then with using AI to create our own music or movies, but for the most part, we will rely on the ingenuity of others. We’re fundamentally dependent on the creativity of others. If you’re not convinced of this, the email below by Steve Jobs explains this far more eloquently than I can.  Despite us having the power to be more creative than ever before, we’ll still be highly dependent on the creativity of others. Even if I can create my own tools with AI, I’d still rather use products or consume content created by people who are far more talented than me. This is where I think we enter a world of hyper-personalisation. Many years ago, personalisation just meant marketers sending mass emails with “Dear Sid”, rather than “Dear Sir or Madam”. Nowadays, we have highly targeted advertising, and companies develop their products to hold our attention. But we all still use the same things – my version of iOS is the same as yours, as is my Gmail and my Slack. We might customise elements of the software differently and the content we’re fed will certainly be different, but the actual building blocks are the same. I’m excited by a world where companies take “co-creating with their customers” to a whole new level. If you think about it, the fact that everyone is fed the same version of an operating system, doesn’t make any sense. We all have different preferences and interact with software differently. So why shouldn’t our operating systems learn from these interactions and self-customise to suit our preferences? The same is true of many software products, and even hardware. The technical challenges of achieving this are immense, but nonetheless, it’s fun to imagine a world where our symbiosis with AI results in us each having highly customised tools that learn from our preferences and feedback. Having said all of this, our symbiosis with technology most likely looks like something I can’t even imagine. The point has been made that AI breaks down the barrier of what an application is. Today, an app or software tool is sort of a packaged container that helps us with certain tasks. AI agents and extreme co-creation both create a blurred line, as they have the ability to perform tasks across disparate domains. If this proves to be true, we may move away from single-purpose apps, to an “OS-level” assistant. Either way, one thing is clear – our interactions with technology are going to shift significantly in the next decade. New business models will emerge, and I can’t wait to back the ambitious founders building them. [1] These are fairly unbaked ideas with many holes to be poked.

TL;DR – The proliferation of content and products (thanks to AI tools), means society is going to become less trusting. In lower-trust societies, trust tends to concentrate around a few entities. To reap the rewards of being one of these trusted entities, companies will need to place more emphasis on their brand. In creating a brand and building trust, both externally and with existing customers, I can’t help but think that marketers and salespeople hold the upper hand. And so, I postulate that we are moving away from the age of the engineer, and into the age of the marketer. In April 2020, as the world was in the throes of the coronavirus, Marc Andreessen famously wrote that It’s Time to Build. Fast forward three years and it’s certainly gotten a lot easier to build, mostly thanks to improved AI tooling. As AI makes every engineer a “10x engineer”, new products will continue to pop up at an unprecedented rate. We’re already seeing this, and there’s no evidence of it slowing down. As with any new technology, it’s always fun to postulate about the impact it’ll have. So, I thought I’d chime in on the conversation. The Engineer The last decade (or two) have been the age of the engineer. Ever since the dot com bubble of the late 90s, great fortunes have been built (and lost) in tech. The nerdy engineers from the early 2000s, hacking away in their college dorms now run multi-billion dollar companies. We’ve even had the emergence of the “tech bro”, a movement arguably spearheaded by the man below.

Prior to the rise of the engineer, we had the age of the financier. Every MBA grad from this era dreamed of working on the trading floor at Goldman Sachs. Bonuses that eclipsed the size of some small countries' GDPs were not unheard of.

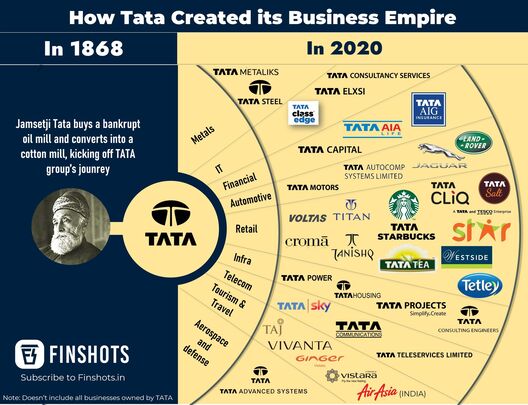

So, what’s next? Within my lifetime, the hottest opportunities for young graduates have seen a transition from investment banking and consulting, to product manager and founder. These areas are still desirable, but layer on the new trend of becoming a content creator and one thing is for sure – the next few years will see more content and more products being built than ever before. The Implication for Startups As it gets easier to build software, more value is created through distribution. For the majority of software companies, and especially for earlier-stage startups, moats have never really come from a technological leap. Elad Gil writes about this in more depth: “Most early-stage startups are not very defensible. Many tech startups will launch an early product within 6-12 months of founding. Teams will initially be 2-5 people with a mix of eng/product/other. Definitionally, it is easy to copy or clone something that has taken a handful of people a handful of months to build.” As it becomes easier to build software, technical moats are eroded even further. This means that a) there are going to be 10 times as many products competing for our limited attention, and b) the only real moat in software will come from engaged users. The Propensity to Trust Going forward, we’ll have more options to choose from and more products competing for our attention. If you’re a creator of software, this means you have more direct competitors and more competing substitutes. To think about how this might play out, I’m going to borrow from Kunal Shah’s framework on high vs. low trust societies. If we step back in time and look at the history of tribes, religions and countries, we can see that in order for trust within a community to grow, they need a good system to detect and punish bad behaviour, whilst rewarding good behaviour. In game theory terms, you need a way to punish the defectors and reward the cooperators. If you can’t identify the defectors, no one knows who to trust and as a result, trust within a society can’t grow. Studies have shown that Eastern societies are generally less trusting than Western societies. In low-trust societies, trust tends to concentrate around a few chosen entities. For example, when a high-trust entity like Tata Group, a leading Indian conglomerate, launches a new product, people will just go out and buy it. Whether it be a car, a fridge, or salt, people will just buy it. This explains why “super apps” are so prolific in Asia – when a high-trust entity launches a new product, people will just use it. The converse is true in the West – if Facebook was to release a dishwasher, people would be highly sceptical.

Marketers – It’s Time to Shine

This brings me to the crux of my argument. A proliferation of new products, many of which will be low-quality, means we are moving to a lower-trust society. To build an enduring business, creating a high-quality brand and earning trust with customers is going to be more important than ever. Within each industry, no matter how niche it is, the companies with the strongest brands are going to be most well-positioned to layer in new products and protect their margins when the lookalikes come knocking. In practice, this means a) creating a strong external brand to attract new customers and potential employees, and b) levelling up support for existing customers. Ultimately, brand is just a proxy for trust [1]. With the inevitable explosion of products, I can’t help but think that those who know how to relentlessly build trust hold the upper hand. This sounds like something that marketing professionals are well placed to do, whether it be an enterprise salesperson, a product marketer, or a community builder. And so, if this line of thinking stands, it would seem that we’re about to enter the age of the marketer.

[1] Tying this back to our game theory concept – building trust with customers can be thought of as a repeated game, where the same players continue to interact with each other. Each interaction between you and your customers can be thought of as a move in this repeated game. The strategies you choose in each interaction will dictate how well you are able to build trust over time. In this sense, incumbents may possess a benefit if they are already deeply progressed into this game, and have made the right moves to build trust.

Setting the Stage If you’re an early-stage founder, you probably don’t care what the Fed or RBA are doing. All this pessimism goes against your fabric. The world of tech is meant to be a world of optimism. But, when reality shifts, unfortunately, so must you. Ahead of us lie a few challenges:

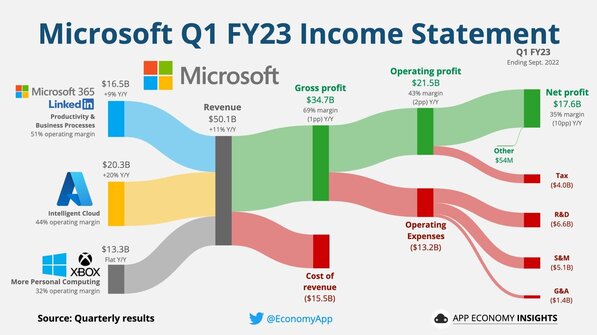

Satya Nadella remarked on Microsoft’s most recent earnings call: "Just as we saw customers accelerate their digital spend during the pandemic, we are now seeing them optimise that spend. Also, organizations are exercising caution given the macro uncertainty."

Nikesh Arora, CEO of Palo Alto Networks remarked: “More scrutiny of tech budgets…is occurring, and that is a significant change from recent times during which the approach has tilted closer to a “blank check” for tech line items.”

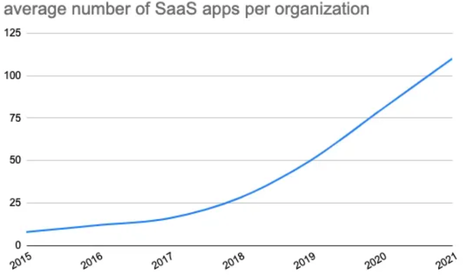

Source: BetterCloud

Source: Crunchbase

Bundling is Back

With all this going on, the term “bundling” is starting to reappear in many people's vocabularies. Jim Barksdale, CEO of Netscape famously said “there are only two ways to make money in business: one is to bundle; the other is to unbundle.” We seem to be in the phase where bundling is in. The easiest example to point to is Rippling. It’s being touted as the next generational software company. Mike Vernal of Sequoia pointed out in an investment memo on Rippling that “as enterprise software has moved to the cloud, we have seen a massive unbundling of products into ever smaller point solutions. Many startups and small businesses have more SaaS subscriptions than employees. While each tool might be individually great, this setup introduces a tremendous amount of administrative complexity. Data is fragmented across many different systems, each with bespoke connectors to dozens of other systems. Managing your business and getting a simple, holistic view of how you’re doing becomes incredibly difficult.” John Luttig, in his notes on Rippling, pointed out that “bundling is Rippling’s accumulating advantage that offsets classical diseconomies of scale. This means that, unlike most growth-stage companies, Rippling’s core metrics improve over time. CAC paybacks decrease. Growth accelerates. Retention improves. Cross-sell rates increase.” I think they’re both right – bundling can be incredibly powerful. They’re also probably right that Rippling will go on to do incredibly well. If you look at a list of the largest public companies in America, you’ll notice that all the B2B software companies have product and revenue diversity. Charts like the one below have become increasingly popular and are a testament to this diversification.

So, yes, bundling is a pretty good long-term strategy. But I also think this renewed interest in bundling misses two key things:

Source: Thursday Threads, Spencer Peterson

This brings me to the crux of the article, and it is well summed up by Packy. In The Good Thing about Hard Things, he wrote “it’s easier than ever to build the average software company – plug into AWS, snap in a bunch of APIs, follow established playbooks – and harder than ever to make it really big. Modularized inputs and playbooks lead to more competition, smaller opportunities, and lower margins.”

Basically, it’s easier to build and tougher to sell. Bundling is a good but an impractical solution for most. So, how do you get a leg up? With my investment hat on, I decided to dive into some strategies that may work well and came up with a potential answer: take a leaf out of the Consumer GTM playbook. I arrived at this conclusion after stumbling upon some analysis from Toplyne. They recently surveyed 1.8m users of bottoms-up software products and found that the magic number is 10 seats. At this point, retention rates inflect upwards and the risk of churn falls considerably. This means that similar to consumer growth teams who spend a lot of time experimenting with acquisition and retention, you should also be rapidly testing new ways of getting to 10 seats. Once you reach this point, you have every chance of growing revenue within an organisation by 10-50x (as the companies in the chart below have done).

Source: Battery

Working Backwards from 10 Users

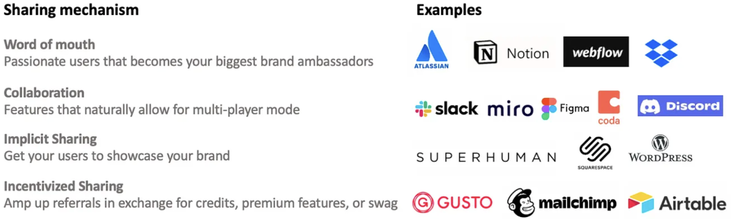

In order for your product to be used by 10 people within an organisation, it will need a sharing mechanism or viral loop. This basically means users share the product with non-users – internally and ideally, externally.

Source: Antoine Nivard and Rosie Chopra

The Viral Loop Deconstructed

David Skok has some great material breaking down the science behind viral marketing. We can roughly think of this in three steps: activation, referrals and conversion.

Source: David Skok

Tactics to Improve Virality

Measuring Virality There’s a lot to unpack here, so I’ll leave you with 3 metrics that are worth taking a look at. If you’re diligent with data-driven experimentation, the trends and outputs from these metrics should be very valuable.

Finally, I’d be remiss if I didn’t acknowledge that I haven’t discussed unit economics or pricing tactics in this article. These obviously have an enormous bearing on your approach and should be looked at in tangent with other decisions.

As always, I’d love to hear thoughts and feedback. You can reach me on LinkedIn or Twitter.

I’ve recently met a number of startup Founders who express regret when asked about their first international hire. The typical response is something along the lines of “our first hire wasn’t great, it set us back a few months, but we’ve learnt a lot from the experience”. After hearing the same thing a few times, I thought it’d be useful to share some of what I’ve learnt.

If you’re an Aussie or Kiwi Founder hoping to build a big business, expanding overseas is often viewed as a potential unlock to a big market. It can be a defining moment for the company, and it’s something you only get to do once. I don’t think I need to convince you that your first hire on the ground is important. The big mistakes I’ve seen are:

The biggest trap I’ve seen Founders fall into is thinking they need to get someone with great connections who’s worked at a big company and knows what it takes to scale a business. I frequently hear things like “we got the ex-Head of Sales at [insert big company] to come on board”. That's great but it's probably not what you need in your first hire. What you really need is someone who is hungry, and who you trust. You want to avoid hiring someone who seems great based on their experience but isn't on board with what it actually means to work in an unstructured environment. During the interview process, these ex-Head’s of will probably convince you that they’re deeply passionate about the problem you’re solving and that they love your product. They’ll also probably say that they’ve spent enough time working at big companies and now want to work on something new and exciting. However, launching internationally is often not as glamorous as it sounds. It means localising your product, talking to customers, researching the market, searching for offices, setting up basic sales processes, and a whole lot more. When I joined an Aussie fintech startup as their first US hire, I spent hours calling various government agencies, speaking to banks, setting up an office and PO box, conducting interviews, and ordering equipment, all whilst being 14 hours behind my colleagues in Australia. Being the first boots on the ground means a lot of multidisciplinary foundational work. This person will be working across sales, operations, product and marketing. This means that they need to learn quickly and be willing to toss aside their Job Description to just get shit done. So what types of people can do that well? The three cohorts of people that come to mind are young consultants, investment bankers, and recent MBA grads. These people likely have a few years of professional experience, they know how to grind and they’re usually hungry. You’ll want to make sure you find someone who also knows how to figure out stuff on the fly. Young people also typically have the added benefit of having more free time. You can usually lure these people away by selling the opportunity. If they’re good, they’ll be given responsibilities years ahead of schedule. You can also typically hire these people at cheaper rates than say, for example, a VP of Sales at Hubspot. Many Founders stretch their budgets to overpay for senior hires, and then regret the decision in a few months. A few other things to keep in mind:

There’s a lot to consider when hiring internationally and much of this advice will vary based on what your company does and the stage at which you’re at. Whilst no hard and fast rules exist, I firmly believe that hiring a hungry generalist who you trust is a great way to seed your overseas operations. As always, I’d love to hear thoughts and feedback. You can reach me on LinkedIn or Twitter.

Part I: Changing Tides

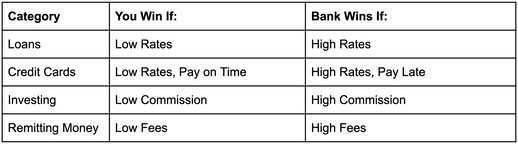

I recently came across a tweet from Anish Acharya that uses game theory as the basis for explaining the changing tides in consumer finance. Inspired by this, I decided to write a breakdown of some areas that are changing, the companies behind the change, and how consumers stand to benefit. This will be a multi-part part series covering student loans, FICO scores, the new alternative investing landscape, real estate, and more. Finance, specifically consumer finance, has always been thought of as a "you win I lose, I win you lose" industry. It's been a zero-sum game – one party must lose in order for the other to win. And this makes sense. At a high level, think of:

What's clear from this table is that there is a serious misalignment of incentives. The bank wins if the consumer loses, and vice versa. As a result, the whole industry has been considered predatory, and many people are skeptical of the large institutions that are, by default, the guardians of our financial assets. And what’s worse is that many people – especially those who are economically disadvantaged or don’t have basic financial literacy – are shut out of the system entirely, or fall victim to a predatory practice.

The good news is that the marriage between finance and technology is flipping this archaic model on its head. We’re moving away from the default of zero-sum, and onto positive-sum, where the consumer and the company can win at the same time. For this to happen, companies must redefine the basic business models that they have relied upon for decades. And it all starts with a better alignment of incentives, where the consumer and the company are both incentivized to strive for the same set of outcomes. In this sense, companies are not competing for a larger slice of the same pie, but are instead competing to capture their share of a pie that they are helping to grow. Put simply, the company wins when you win. Better outcomes mean that for the first time in history, individuals who traditionally did not have access to the financial infrastructure, are finally being brought into the fray. More people can access quality financial products, and live better lives. Here are some of the most striking examples of business models eschewing the positive-sum game mindset:

There are many examples of both predatory practices and the ways in which fintech companies are changing this dynamic. We'll delve into them in the following chapters, starting with the power of the collective.

Part II: United We Stand

The concept of buying in bulk is not foreign to us. In fact, it’s so commonplace that we’ve almost come to expect it. It’s a simple principle – purchase large quantities and be rewarded with a discount. Unfortunately, this mindset has not ported itself over to the lonely world of personal finance. Think about the last time you got a loan. In fact, think about any time you’ve ever gotten a loan. I’d be willing to bet that it was purely an individual process. You might have gone to a few banks (or credit providers), shopped around for the best rates, and negotiated your hardest – but at the end of the day – it was you, the little guy vs. the world. Put differently, with today’s infrastructure, each user is trying to optimize his/her own financial decisions independently. As a result, the big banks and credit providers retain all the power when negotiating. They have the ability to set terms, rates, and fees – they basically dictate the entire process. The consequences of this fragmentation are that consumers lose out. And in some “less efficient” markets, the imbalance of power between the two parties lends itself to extreme pricing power. One such case is the international student loan market, where rates in excess of 15% are not rare, even for creditworthy applicants. But what if the market wasn’t so fragmented? What if that same concept of bulk buying was translated over to the personal finance arena? Well, one startup is doing just this. Juno (formerly LeverEdge) helps groups of students band together and negotiate reduced student loan rates, by acting as a collective bargaining unit. Juno was started by two students at Harvard Business school, which currently boasts an annual attendance cost of ~$110K. Instead of one powerless student approaching 10 banks and hoping for the best rate, an entire class of students can approach a few banks and in turn, force them to compete to offer the lowest rates. Bring the volume and get the best deals. But for Juno to be successful, they need to amalgamate enough loan volume such that their value proposition is compelling for creditors. Sure enough, their first batch had over 700 MBA students with $26M in loan applications. With that volume and through their auction process, Juno estimates that they were able to save each student an average of $15,000 over the life of their student loan. I’m fascinated with this model because of its simplicity. Many innovative startups in the student loan space currently do one of two things. They either provide advice (like a financial advisor) or they are building out new infrastructure, as is the case with income share agreements (which I’ll cover next). There’s nothing wrong with either of these models, but Juno is unique because it has opted to follow its own path, by simply uniting people in the same situation. In this sense, Juno is taking securitization into their own hands. Securitization is the process of pooling various financial assets into one group and then selling them to investors. For example, mortgage-backed securities (which were in part responsible for the 2008 financial crisis) are pools of home loans that investors buy. Investors buy them because, in theory, they provide steady cash flow. Banks sell them to investors because it helps them to de-risk their balance sheets. Juno is taking ownership of this pooling process and allowing the consumers to benefit from it. If we think about this in terms of the game theory concept I introduced earlier – this is truly a positive-sum game. Students win because they get lower rates and save money. Banks win because instead of individually negotiating with – in this example – 700 individual parties, they just negotiate with Juno and get a $26M ticket. The best part is that Juno makes money by charging banks a syndication fee, meaning it is free for students – an ultimate win-win situation. Currently, Juno has raised ~$2.5M, has a network of 30K+ students, and has originated over $100M in student loans. Going forward, I think their potential market is huge. In addition to expanding into adjacent markets (like law & undergraduate students), they’re also diversifying their product base, by offering refinancing and insurance solutions. Down the line, they could even move into the credit card and real estate arenas. However you want to describe this idea – whether it be group purchasing power, collective bargaining, or consumer-side securitization – I think the concept has legs. I’m excited to see where it goes and how it evolves. Next up, I’m going to provide a backdrop for the current state of the student loan market in the US. Following this, we’ll delve into some general approaches to this problem and hone in on a fascinating structural solution that is quickly gaining momentum – the Income Share Agreement. If you’d like to read more about Juno, here are some handy links:

Part III: Student Loans Reimagined

The student loan market in the US is hugely problematic. There’s $1.5T in outstanding debt and 40% of borrowers are expected to default by 2023. People are burdened by debt, and others simply cannot access education because of the financial barrier. This is a huge weight on the financial system, and repercussions will trickle down to the everyday American. A Quick Primer on Student Loans In the US, there are two primary types of loans: federal and private. Federal loans are provided by the government, meaning they’re cheaper and more flexible. Private loans are used in cases where federal loans do not cover the entire funding amount. Because federal funding is limited, many people end up relying on private loans. Private loans generally have higher rates and often require a cosigner. The first wave in re-imagining student loans came from companies like SoFi and CommonBond. They offered student loans and refinancing at lower rates than traditional companies (like a Sallie Mae) and also offered a better customer experience. Students finally had friendlier options. But the fundamental model for student loans did not change – the new players just added an increased element of competition. Where It Gets Interesting Some countries (like Germany and Australia) have used Income Share Agreements (ISAs) or a similar model, like an income-contingent repayment plan for a long time. And for the most part, they’ve worked pretty well. As a proud Australian, it’s only appropriate that I focus on the system I grew up with. HECS-HELP, as it’s known, is a system for Australian citizens studying at universities in Australia. Basically, the government gives you a loan to help you pay for your education. The loan is interest-free but indexed to inflation, so it’s really cheap. Once you start working and reach a minimum income threshold, you start repaying this loan directly through your paycheck – similar to how taxes are withheld. The thresholds and repayment percentages are set every year. The minimum income threshold for 2020-21 is $46,620. The system is certainly not perfect, but it’s well understood by Australians and makes education a lot more accessible. Getting an interest-free loan is a once-in-a-lifetime offer, and so many students take advantage of it. So far, it has not been a huge burden to the financial system. The Private Solution A number of startups in the US are trying to tackle the issue of student loans. Many have had moderate success, but the industry is still in its first innings. From what I’ve seen, there a few approaches that companies are taking, including offering:

The Financing Solution Of the three solutions being presented, this first one is the most complicated. There’s a lot to break down and there are many companies in the space, but I’m going to try and keep it simple. For decades, students in the US have taken out loans to pay for college. In 1955, the famed economist Milton Friedman introduced the concept of an ISA. The idea had some early adopters (like Yale University), but only in recent years has it begun to gain traction. Here’s how it works: with loans, you pay regardless of how much you earn. With ISAs, you receive funding to pay for your education and in exchange, agree to share a percentage of your future income with your lender. The terms of the ISA are primarily dictated by 5 variables:

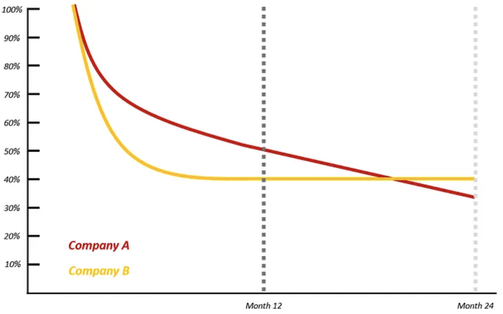

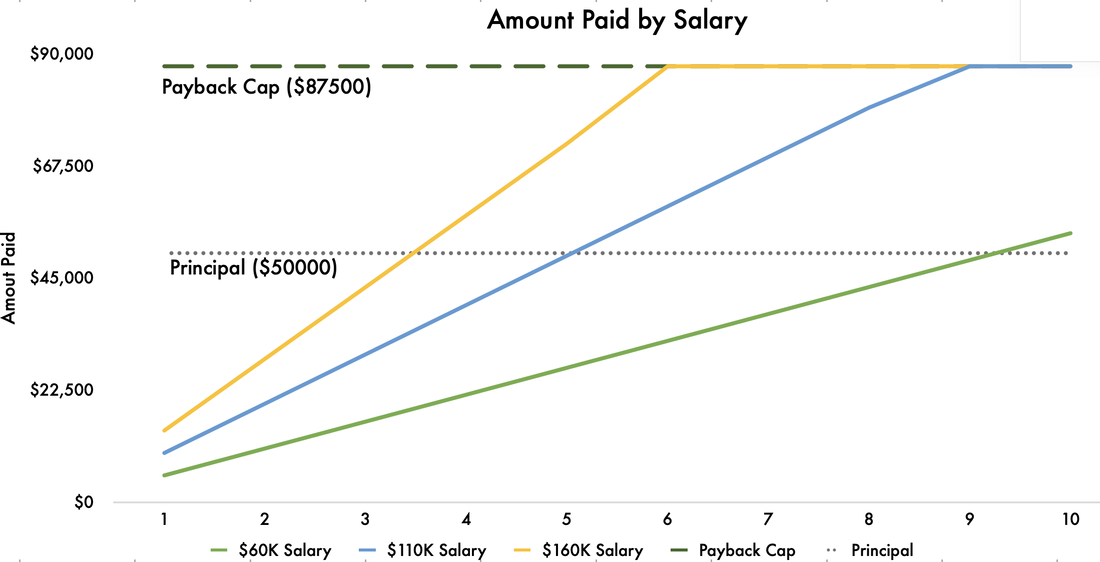

You begin payments once your income exceeds the income threshold, and you continue making payments until either the payback period expires or the payback cap is reached. In the graph below, you can see a simple example of how this works in practice for a $50k loan, 9% income share and 10 year payback period. The person earning $60k only pays back a little more than the original principal, whilst those on higher salaries reach the payback cap. The example does not take into account the fact that salaries generally rise over time.

But there are tons and tons of questions relating to ISAs. Some are more philosophical in nature, whilst others are purely related to the mechanics of how they work. Scroll down to the “Criticisms and Concerns” section of this article if this is something that interests you.

Putting aside these concerns are a few brave startups, such as Avenify, Blair, Edly, and Lumni. There are many more in the space, but they all tend to differentiate themselves using some combination of the following models:

As far as I see it, the adoption of ISAs will be a major structural shift in how student loans are viewed. They’re complex and there currently isn’t enough data to make a call on how successful they will be. As these startups continue to generate data from their first few batches of ISAs, underwriting expectations will surface and we will be able to judge their efficacy. Ultimately, if ISAs are successful, the $1.5T debt burden of student loans will stop growing. The value of a school will not be based on arbitrary rankings, but instead on the outcomes they achieve for their students. And most importantly, more students will be able to access education. The Primary Education Solution The most striking example here is Lambda School. They offer students a high-quality CS education through an ISA model. Students pay no tuition upfront, and agree to pay back 17% of their post-graduation income for two years, but only once they’re making $50,000 or more. If they don’t get a high-paying job after 60 months of deferred payments, they pay nothing. As Lambda School says: “this paradigm-shifting model allows us to align the incentives of the school with the incentives of our students – and we all win when our graduates succeed.” Whilst there are both staunch advocates and critics of Lambda School, it can definitely open up doors for students who are interested in landing high-paying jobs at prestigious tech companies. And most notably, their program is only 9 months long – leading to a much higher ROI compared to the typical 4-year college degree. If you look at recent YC batches, there are a number of companies trying to replicate this model, for different geographies and industries. These startups are betting on people opting for outcome-focused models like Lambda or Udemy, and avoiding the costly 4-year college experience. One thing to note – this essay does not take a philosophical position on the role of a 4-year college experience. That’s a whole other ball game – one that is both important and highly complex. Regardless of your take on education, there’s no doubt that the Lambda School concept is an interesting marriage between education and financing. And above this, innovation in education is truly a win-win for students, who are the ultimate beneficiaries as they have both more options for education, and a better way of financing it. Advice One of the biggest problems in consumer finance historically has been a lack of access to quality education. Most people don’t like dealing with their finances – it’s stressful, complicated, and easier to punt on. Unfortunately, those from disadvantaged backgrounds are the worst affected, as they typically have both less money, and less access to good financial education. This causes a circular loop to form, resulting in compounding financial issues and thousands of dollars being lost in the long run. Given that we are now truly living in the information age, it’s no surprise that the internet has so much information about managing individual finances. The famous subreddit, r/personalfinance has a ton of information about budgeting, saving, getting out of debt, investing, retirement planning, and more. But despite it now being easier than ever to access information on handling finances, the problem persists. Companies like NerdWallet make it easier to evaluate options for things like credit cards and student loans, but there are 2 primary issues as I see it:

On the second point – everyone has their own unique situation and unless you have hours upon hours to spend sifting through the web, it’s very hard to find personalized advice. From my experience as an Australian working in New York, the best advice I’ve received has either come from professional experts (like accountants) who are very expensive, or other Aussies in the same boat as I am. That’s where a company like Summer comes into play. Summer is a public benefit corporation that is on a mission to act as a “trusted advisor” to student loan borrowers. From Summer Co-Founder, Will Sealy, “we’re trying to create the software that democratizes [student loan] expertise, that gets the expertise into the hands of the end consumer, who might not be able to afford an accountant”. Basically, students enter information about their personal finances, Summer evaluates thousands of financing options and then recommends the best path forward. They’re solving the problem of not having personalized information. The best part is that this service is free to students – instead, Summer sells through enterprises and other organizations that can offer the product as a benefit to employees. A positive-sum solution. There are other startups in this space, like Mos, which helps students get every dollar of financial aid they qualify for, by simplifying the process of applying to government aid and scholarships. Another startup, Pillar, helps students understand and pay off their debt. Their app connects with a student loan servicer and bank, and then makes personalized suggestions based on loan amount, income, and spending. As the app finds ways for students to make a dent in their overall debt, it will send alerts with the proper advice. The overall takeaway is that whilst these startups are not laying a new foundation for how student loans are issued, they are using the power of data to provide individuals with personalized advice, by looking at thousands of options and presenting the best ones. In this sense, they are like NerdWallet 2.0 in that they don’t just present information, but they actually use your inputs to offer tailored outputs. And, for the most part, they only get paid if you save money i.e. they only capture a percentage of the value they create. Conclusion Student loans – and ISAs in particular – are deeply complex. Whilst there is no doubt that structural change is required in the student loan market, it remains to be seen what the most effective solutions will be. Some closing thoughts:

Finally, I would be remiss if I didn’t mention this – the student loan market is extremely complex. This article might feel like a stream of consciousness and that’s because there’s simply too much to cover, and so much that I am yet to understand. Any mistakes, oversights, counter-arguments, or questions – please feel free to reach out to me. You can contact me via email or Twitter. Following the recent debacle concerning international students and their ability to study in the U.S., I wanted to pen down my personal thoughts on the issue.

It is well-known that international students are money-making machines for the United States. As a collective, we contributed over $41 billion to the U.S. economy in the 2018-19 academic year. This ranks as the nation’s fifth largest services export industry, ahead of business travel and telecommunications equipment. The relationship between international students and the U.S. has always been a win-win. For the privilege of being educated in the land of the free, we pay handsomely. In return, we are afforded amazing opportunities. For universities, the benefits are many. International students typically pay full tuition, keep classes full, and increase patent output (which boosts rankings). The economy benefits too. International students graduate and get high paying jobs in fields like technology. They pioneer research. And they start companies. A 2018 study by the National Foundation for American Policy found that nearly a quarter of the billion-dollar startups in the U.S. had a founder who was an international student. Think of companies like SpaceX ($36B), Stripe ($35B), Robinhood ($8B) and Cloudflare ($8B). All were started by international students. The point of all this is that international students create immense value for the American economy and its people. But lately, the number of international students in the U.S. has been declining. In the 2018-19 school year, U.S. colleges reported a decline in international undergraduates, ending 12 consecutive years of growth. This should warrant concern. International students paying full tuition help keep universities financially afloat by subsidizing American students on financial aid. Tech companies rely on international talent to build innovative technologies. Even a small drop in the number of international students will cost the American economy billions of dollars. The COVID-19 pandemic is not helping. The American Council on Education estimates that international enrollment will drop 25% in the coming academic year, as students face uncertainty over visa approvals and the status of Fall classes. If students can't be on campus, many of the intangibles that come with an American education vanish, and that seventy-thousand-dollar price tag per year suddenly feels a lot steeper. University administrators are worried. Every lost international student “represents a four-year hit. Those students would typically be enrolled for four years, so that’s a negative on the balance sheet for several years” said Daniel Hurley, chief of the Michigan Association of State Universities. But there is a larger issue at hand. It’s no secret that the U.S. has not handled this pandemic well. Famed economist Joseph Stiglitz has said that this crisis has left the U.S. looking like a “third world” country. The political climate has already become more hostile to international students. If this trajectory continues, will parents be able to justify the monumental expenses that come with sending a child to the U.S.? Despite this, I’m an advocate of the American way of education. My four years at Duke have provided me with ample opportunities both in and out of the classroom, and have facilitated immense personal growth. The good news for colleges is that this pandemic provides the perfect backdrop for making the international student experience better. As Pulitzer-prize winning journalist Charles Duhigg puts it, crises should be used as opportunities to remake organizational habits, because it is during these times that habits are most malleable. Christina Paxson, the President of Brown University hit the nail on the head when she said that “the reopening of college campuses in the fall should be a national priority”. But I urge institutions worried about their international student enrollment numbers to go one step further. Realize that being a student in college is tough. Being an international student in college is even tougher. But being an international student dealing with a global pandemic is unprecedented. Colleges should use the malleability this pandemic affords as a launching pad for change – to give these students the experience they want (and deserve), so that the productive exchange between international students and America can continue for years to come. It’s January 2020, and I am about to start my final semester at Duke. After three and a half grueling years studying engineering, I’m ready for a change of pace. This semester’s going to be a breeze. I’m in easy classes and do not have the pressure of needing to find a job.

As I walk around campus, I can’t help but notice stressed underclassmen worrying about exams, papers, and internships. It’s a constant one-up competition where they brag about how little they slept, and how much work they managed to do. Productivity is a social signal. Three months later, classes are canceled and campus is deserted. But my Zoom calls with peers don’t feel that different. Everyone is talking about how little work they get done at home. Geographically isolated, but united in the quest for productivity. I go on Twitter and it’s the same thing. My feed is full of people talking about their productivity levels. Some like working from home, others don’t. Some use the newfound free time to execute on their dreams. Others feel disillusioned and sit on the couch complaining about how hard it is to get anything done at home. As an international student, I’m naturally stressed. I’m not from here. My group chat with other internationals is blowing up. Duke wants us off campus, but we don’t know if it’s even safe to fly home. And if it is, where do I get the money to pay for the flight? What’s going to happen to my job? I’ve already signed a 1-year lease on my New York apartment. If I leave the country will I be allowed back in? And my visa status? My first thought is – I need to get on top of all this. If I can just sit down for a few hours and be productive, I can get a headstart on all these issues and I’ll feel better. But just like my peers, I can’t get anything done. I turn to my phone and come across photos from my freshman year and I start to reminisce about the good old days. Oh, how I miss those days. It’s during this moment of reflection that I realize how we, as humans, only appreciate things in hindsight. We’re not accustomed to living in the moment. That’s why all those underclassmen are stressed about exams and internships. That’s why I’m stressed about my job. In that moment it starts making sense to me. We’re so infatuated with productivity because we’re so worried about the future. Maybe that’s why so few people follow their passions. Peter Thiel hit the nail on the head when he said: “higher education is the place where people who had big plans in high school get stuck in fierce rivalries with equally smart peers over conventional careers like management consulting and investment banking.” Duke is a small sample size but wow, almost everyone I know is working for a bank, a consulting firm, or a big tech company (myself included). Students come to college with big dreams, but this culture of worrying about the future forces people to brush aside the things they love. We delay pursuing passions in order to secure our futures so that we can provide for ourselves and our families. In the process of doing so, we tell ourselves that once we’re comfortable, once we’re settled down, then we’ll finally do what we love. But by the time that comes around, most people are tired, burnt out, and don’t have the energy. As college students, we should learn to embrace our naivety. At this juncture in our lives, we’re the most passionate and most willing to experiment that we’ll ever be. And the timing is perfect. The current dislocation in the world provides the perfect backdrop for us to make change, no matter the size. Let’s shift our focus away from productivity for productivity’s sake. Being productive for the sake of it gives us a false sense of accomplishment. Sure, we feel good after a busy day, after we’ve seemingly done a lot. But I urge my peers to rethink productivity. Let us veer off the beaten path, let us zone in on pursuits that provide genuine satisfaction, and let us use the problems that this pandemic has exacerbated as a launching pad for change. Success stories come in many different forms. Whether it be something you read, a friend who has achieved great success, or an ad that inspires you to be better - these stories are everywhere. Products are sold through the success that they have enabled their customers to achieve. So often have I been a victim of these stories - some inspire me to get in amazing shape, some inspire me to start the next unicorn, and others might inspire me to read 50 books a year like Bill Gates. But in most cases, we are only sold the final product. In reality, achieving goals takes incremental persistence. You can't wake up and run a marathon, you need to practice - you need to keep chipping away at it. And that's why habits are important. Good habits put you on the path of incremental improvement and can culminate in something amazing. Setting So habits are important. But making a habit stick is difficult. We've all made New Years Resolutions, only to break them within a week. And that’s because many people set unreasonable expectations for themselves. When it comes to habits, I don't think the whole "shoot for the moon and land amongst the stars" thing works. That’s because if you don't hit your goals, it becomes easier to just put them off. Reasonable action > drastic action. A nice framework I came across from Matt D’Avella: ask yourself how confident you are in achieving a certain habit. Example: On a scale of 1-10, how confident do you feel about going to the gym 5 times this week? If your confidence level is at 7 or less, revise the frequency downward. Keep going until this number exceeds 7. Starting off small is perfectly fine because you don't want the task to seem too daunting. Tracking Setting habits is one thing, but you must also track them. It's the most concrete way to measure progress and there are many ways to do this. I personally use the Way of Life App. Basically, you enter the habits that you want to develop. For each day there is a box that you color: 🟩 (yes I did it), 🟥(no I didn't do it) or ⬜️(I didn't plan to do it). Some examples of how I use it:

As someone who enjoys numbers, I frequently check my trend to see how it compares with previous weeks. This is how I guarantee improvement. As you improve, you can revise your goals upwards.

2 Day Rule This is a simple rule, but it has really helped me. For habits I intend to do frequently (reading, working out), I make sure I don't skip 2 consecutive days. Sometimes life gets in the way and you have to skip a day. But if you break a habit twice in a row, it becomes much harder to get back into it - because putting it off becomes the new default. Having done this for a while, I've found that certain habits have become so ingrained that my day feels incomplete until I get that green box. Final Thoughts Everyone has a different system and you have to find what works well for you. A few things that I have noticed:

Rec'd was a social app for friends to share food & drink recommendations and was the first "startup" that I ever built. I put startup in quotation marks because I'm not sure at what stage something is considered a startup. I'm writing this because I wanted to reflect on the experience and make sure rec'd wasn't forgotten.

No More KFC In Fall 2018, I was studying abroad in Madrid and having the time of my life. One of the best parts of the experience was the weekend trips to new cities. One night in Budapest, we were struggling to find a place to eat dinner. Yelp, TripAdvisor and Google yielded nothing. Their websites were cluttered, there were thousands of reviews from random people and even the McDonald's down the road had a 5-star rating. By the time we found a place, it was too late. We ended up eating dinner at KFC. The following weekend in Paris we were determined not to find ourselves at KFC again. We wanted authentic and affordable dining experiences. So we asked our friends who had already visited Paris for recommendations. We ended up having some of the most memorable dining experiences from our entire time abroad. High off our success, we headed into Rome the following week equipped with recommendations. And we left satisfied, after some amazing meals. Recommendations Run Supreme After these experiences we realized two things:

We wanted to bridge this gap. Our solution? A social app that allowed people to share travel recommendations with only their friends. Basically, users could:

We sat on the idea for a while - refining it, strategizing about how we would overcome the chicken & egg problem, and making prototypes. The following semester at Duke, we continued this process until we developed the conviction we needed to proceed. During the summer, we started using Glide (a no-code tool for apps) to build our MVP. Our goal was to target the highest-need users, and get honest feedback. For this reason, we decided to brand the MVP as a shared resource for Duke students studying abroad. Whilst finalizing the MVP, we began seeding the app with recommendations from friends who studied abroad. Our next goal was to get the app in the hands of Duke students abroad. We posted in the Class of 2021’s Facebook group and had a really positive response, with over 100 students signing up in 2 days. We felt validated. It had taken us only a few weeks to build the MVP and launch. Denouement This is where the problems start. Our first mistake was not being able to track usage. All we knew was that 40% of people who signed up logged on to the app. Beyond that, we couldn't gauge activity. A few people added reviews but the majority didn't. Maybe they were using the app for recommendations but not adding places themselves? We couldn’t tell. We tried to get in touch with users (emails & surveys) but didn't have much success. This was our second mistake. We had no way of contacting our users directly via the app. Around the same time, we received a rejection from YC. We were disappointed but not surprised. Our video interview had gone poorly. For the next few months, things felt stagnant. We were struggling to get user validation and as a result, weren't sure whether to proceed with the development of a real app. Ultimately, we decided to move on to another idea - something that we felt solved a bigger problem (stay tuned). I learned a ton from this experience and whilst I still feel there is a gap in the market, I am also acutely aware of how difficult execution can be. Three takeaways:

Netflix's docuseries Inside Bill's Brain: Decoding Bill Gates opens with him reading the Minnesota state budget. Beside him lie 37 more state budgets. It's a fitting introduction for a man who spends a significant portion of his waking hours reading. It is generally well accepted that reading is a good habit. Almost every successful person says so. So how do we make sure we're actually engaging with the books we read? During my semester abroad in Madrid, I found myself with a lot more free time. I used this time to read more, and ended up finishing over 10 books during the semester. In doing this, I was confronted with 2 problems:

Paul Graham doesn't have a problem with this. Reading and experience train your model of the world. And even if you forget the experience or what you read, its effect on your model of the world persists. Your mind is like a compiled program you've lost the source of. It works, but you don't know why. — Paul Graham This gave me some comfort but I wanted to do better, especially with the engaging aspect. In other words, I wanted to be an active reader, not a passive one. But how? Many people (Gates, Newton, Fermat) write in the margins of their books. I tried doing this for a while but I often didn't have enough space, or I didn't own the book. So, I decided to modify this technique by using post-it notes. Basically, whenever I come across something intriguing, something I disagree with or a new idea of my own - I write it down on a post-it and also note down the page number. I stick the post-its on the inside cover of the book. Check it out below.  There's no algorithm for what to write down, it's really just based on your judgment. Many times I'll summarize an interesting argument that spans multiple pages into a sentence or two.

In a week's time, I revisit the book and try to write about it using my notes as reference. Again, there's no format on what to write - I just pretend I'm giving a friend my take on the book. This is the purpose of the bookshelf section of my website, it's just a way for me to better engage with the books I read and well, give you my take on the book. This technique certainly won’t work for everyone. I know many people use Kindles, where this analog approach isn't even feasible. Either way, I highly recommend developing your own technique to become a more active reader. Feel free to use this technique as your first iteration! |