|

Part I: Changing Tides

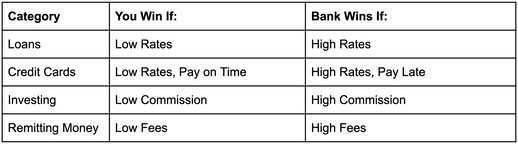

I recently came across a tweet from Anish Acharya that uses game theory as the basis for explaining the changing tides in consumer finance. Inspired by this, I decided to write a breakdown of some areas that are changing, the companies behind the change, and how consumers stand to benefit. This will be a multi-part part series covering student loans, FICO scores, the new alternative investing landscape, real estate, and more. Finance, specifically consumer finance, has always been thought of as a "you win I lose, I win you lose" industry. It's been a zero-sum game – one party must lose in order for the other to win. And this makes sense. At a high level, think of:

What's clear from this table is that there is a serious misalignment of incentives. The bank wins if the consumer loses, and vice versa. As a result, the whole industry has been considered predatory, and many people are skeptical of the large institutions that are, by default, the guardians of our financial assets. And what’s worse is that many people – especially those who are economically disadvantaged or don’t have basic financial literacy – are shut out of the system entirely, or fall victim to a predatory practice.

The good news is that the marriage between finance and technology is flipping this archaic model on its head. We’re moving away from the default of zero-sum, and onto positive-sum, where the consumer and the company can win at the same time. For this to happen, companies must redefine the basic business models that they have relied upon for decades. And it all starts with a better alignment of incentives, where the consumer and the company are both incentivized to strive for the same set of outcomes. In this sense, companies are not competing for a larger slice of the same pie, but are instead competing to capture their share of a pie that they are helping to grow. Put simply, the company wins when you win. Better outcomes mean that for the first time in history, individuals who traditionally did not have access to the financial infrastructure, are finally being brought into the fray. More people can access quality financial products, and live better lives. Here are some of the most striking examples of business models eschewing the positive-sum game mindset:

There are many examples of both predatory practices and the ways in which fintech companies are changing this dynamic. We'll delve into them in the following chapters, starting with the power of the collective.

Part II: United We Stand

The concept of buying in bulk is not foreign to us. In fact, it’s so commonplace that we’ve almost come to expect it. It’s a simple principle – purchase large quantities and be rewarded with a discount. Unfortunately, this mindset has not ported itself over to the lonely world of personal finance. Think about the last time you got a loan. In fact, think about any time you’ve ever gotten a loan. I’d be willing to bet that it was purely an individual process. You might have gone to a few banks (or credit providers), shopped around for the best rates, and negotiated your hardest – but at the end of the day – it was you, the little guy vs. the world. Put differently, with today’s infrastructure, each user is trying to optimize his/her own financial decisions independently. As a result, the big banks and credit providers retain all the power when negotiating. They have the ability to set terms, rates, and fees – they basically dictate the entire process. The consequences of this fragmentation are that consumers lose out. And in some “less efficient” markets, the imbalance of power between the two parties lends itself to extreme pricing power. One such case is the international student loan market, where rates in excess of 15% are not rare, even for creditworthy applicants. But what if the market wasn’t so fragmented? What if that same concept of bulk buying was translated over to the personal finance arena? Well, one startup is doing just this. Juno (formerly LeverEdge) helps groups of students band together and negotiate reduced student loan rates, by acting as a collective bargaining unit. Juno was started by two students at Harvard Business school, which currently boasts an annual attendance cost of ~$110K. Instead of one powerless student approaching 10 banks and hoping for the best rate, an entire class of students can approach a few banks and in turn, force them to compete to offer the lowest rates. Bring the volume and get the best deals. But for Juno to be successful, they need to amalgamate enough loan volume such that their value proposition is compelling for creditors. Sure enough, their first batch had over 700 MBA students with $26M in loan applications. With that volume and through their auction process, Juno estimates that they were able to save each student an average of $15,000 over the life of their student loan. I’m fascinated with this model because of its simplicity. Many innovative startups in the student loan space currently do one of two things. They either provide advice (like a financial advisor) or they are building out new infrastructure, as is the case with income share agreements (which I’ll cover next). There’s nothing wrong with either of these models, but Juno is unique because it has opted to follow its own path, by simply uniting people in the same situation. In this sense, Juno is taking securitization into their own hands. Securitization is the process of pooling various financial assets into one group and then selling them to investors. For example, mortgage-backed securities (which were in part responsible for the 2008 financial crisis) are pools of home loans that investors buy. Investors buy them because, in theory, they provide steady cash flow. Banks sell them to investors because it helps them to de-risk their balance sheets. Juno is taking ownership of this pooling process and allowing the consumers to benefit from it. If we think about this in terms of the game theory concept I introduced earlier – this is truly a positive-sum game. Students win because they get lower rates and save money. Banks win because instead of individually negotiating with – in this example – 700 individual parties, they just negotiate with Juno and get a $26M ticket. The best part is that Juno makes money by charging banks a syndication fee, meaning it is free for students – an ultimate win-win situation. Currently, Juno has raised ~$2.5M, has a network of 30K+ students, and has originated over $100M in student loans. Going forward, I think their potential market is huge. In addition to expanding into adjacent markets (like law & undergraduate students), they’re also diversifying their product base, by offering refinancing and insurance solutions. Down the line, they could even move into the credit card and real estate arenas. However you want to describe this idea – whether it be group purchasing power, collective bargaining, or consumer-side securitization – I think the concept has legs. I’m excited to see where it goes and how it evolves. Next up, I’m going to provide a backdrop for the current state of the student loan market in the US. Following this, we’ll delve into some general approaches to this problem and hone in on a fascinating structural solution that is quickly gaining momentum – the Income Share Agreement. If you’d like to read more about Juno, here are some handy links:

Part III: Student Loans Reimagined

The student loan market in the US is hugely problematic. There’s $1.5T in outstanding debt and 40% of borrowers are expected to default by 2023. People are burdened by debt, and others simply cannot access education because of the financial barrier. This is a huge weight on the financial system, and repercussions will trickle down to the everyday American. A Quick Primer on Student Loans In the US, there are two primary types of loans: federal and private. Federal loans are provided by the government, meaning they’re cheaper and more flexible. Private loans are used in cases where federal loans do not cover the entire funding amount. Because federal funding is limited, many people end up relying on private loans. Private loans generally have higher rates and often require a cosigner. The first wave in re-imagining student loans came from companies like SoFi and CommonBond. They offered student loans and refinancing at lower rates than traditional companies (like a Sallie Mae) and also offered a better customer experience. Students finally had friendlier options. But the fundamental model for student loans did not change – the new players just added an increased element of competition. Where It Gets Interesting Some countries (like Germany and Australia) have used Income Share Agreements (ISAs) or a similar model, like an income-contingent repayment plan for a long time. And for the most part, they’ve worked pretty well. As a proud Australian, it’s only appropriate that I focus on the system I grew up with. HECS-HELP, as it’s known, is a system for Australian citizens studying at universities in Australia. Basically, the government gives you a loan to help you pay for your education. The loan is interest-free but indexed to inflation, so it’s really cheap. Once you start working and reach a minimum income threshold, you start repaying this loan directly through your paycheck – similar to how taxes are withheld. The thresholds and repayment percentages are set every year. The minimum income threshold for 2020-21 is $46,620. The system is certainly not perfect, but it’s well understood by Australians and makes education a lot more accessible. Getting an interest-free loan is a once-in-a-lifetime offer, and so many students take advantage of it. So far, it has not been a huge burden to the financial system. The Private Solution A number of startups in the US are trying to tackle the issue of student loans. Many have had moderate success, but the industry is still in its first innings. From what I’ve seen, there a few approaches that companies are taking, including offering:

The Financing Solution Of the three solutions being presented, this first one is the most complicated. There’s a lot to break down and there are many companies in the space, but I’m going to try and keep it simple. For decades, students in the US have taken out loans to pay for college. In 1955, the famed economist Milton Friedman introduced the concept of an ISA. The idea had some early adopters (like Yale University), but only in recent years has it begun to gain traction. Here’s how it works: with loans, you pay regardless of how much you earn. With ISAs, you receive funding to pay for your education and in exchange, agree to share a percentage of your future income with your lender. The terms of the ISA are primarily dictated by 5 variables:

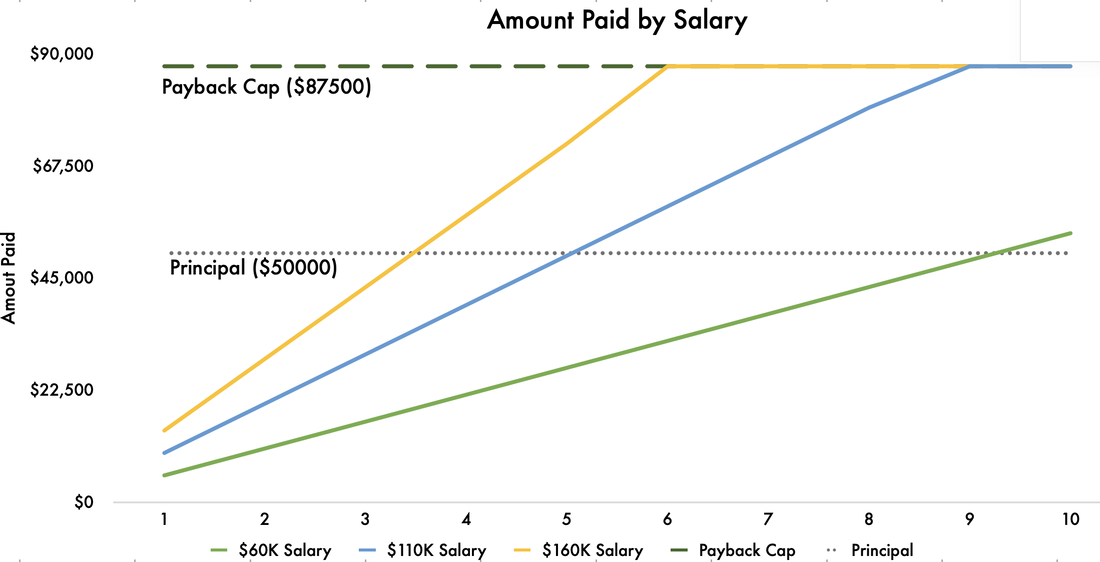

You begin payments once your income exceeds the income threshold, and you continue making payments until either the payback period expires or the payback cap is reached. In the graph below, you can see a simple example of how this works in practice for a $50k loan, 9% income share and 10 year payback period. The person earning $60k only pays back a little more than the original principal, whilst those on higher salaries reach the payback cap. The example does not take into account the fact that salaries generally rise over time.

But there are tons and tons of questions relating to ISAs. Some are more philosophical in nature, whilst others are purely related to the mechanics of how they work. Scroll down to the “Criticisms and Concerns” section of this article if this is something that interests you.

Putting aside these concerns are a few brave startups, such as Avenify, Blair, Edly, and Lumni. There are many more in the space, but they all tend to differentiate themselves using some combination of the following models:

As far as I see it, the adoption of ISAs will be a major structural shift in how student loans are viewed. They’re complex and there currently isn’t enough data to make a call on how successful they will be. As these startups continue to generate data from their first few batches of ISAs, underwriting expectations will surface and we will be able to judge their efficacy. Ultimately, if ISAs are successful, the $1.5T debt burden of student loans will stop growing. The value of a school will not be based on arbitrary rankings, but instead on the outcomes they achieve for their students. And most importantly, more students will be able to access education. The Primary Education Solution The most striking example here is Lambda School. They offer students a high-quality CS education through an ISA model. Students pay no tuition upfront, and agree to pay back 17% of their post-graduation income for two years, but only once they’re making $50,000 or more. If they don’t get a high-paying job after 60 months of deferred payments, they pay nothing. As Lambda School says: “this paradigm-shifting model allows us to align the incentives of the school with the incentives of our students – and we all win when our graduates succeed.” Whilst there are both staunch advocates and critics of Lambda School, it can definitely open up doors for students who are interested in landing high-paying jobs at prestigious tech companies. And most notably, their program is only 9 months long – leading to a much higher ROI compared to the typical 4-year college degree. If you look at recent YC batches, there are a number of companies trying to replicate this model, for different geographies and industries. These startups are betting on people opting for outcome-focused models like Lambda or Udemy, and avoiding the costly 4-year college experience. One thing to note – this essay does not take a philosophical position on the role of a 4-year college experience. That’s a whole other ball game – one that is both important and highly complex. Regardless of your take on education, there’s no doubt that the Lambda School concept is an interesting marriage between education and financing. And above this, innovation in education is truly a win-win for students, who are the ultimate beneficiaries as they have both more options for education, and a better way of financing it. Advice One of the biggest problems in consumer finance historically has been a lack of access to quality education. Most people don’t like dealing with their finances – it’s stressful, complicated, and easier to punt on. Unfortunately, those from disadvantaged backgrounds are the worst affected, as they typically have both less money, and less access to good financial education. This causes a circular loop to form, resulting in compounding financial issues and thousands of dollars being lost in the long run. Given that we are now truly living in the information age, it’s no surprise that the internet has so much information about managing individual finances. The famous subreddit, r/personalfinance has a ton of information about budgeting, saving, getting out of debt, investing, retirement planning, and more. But despite it now being easier than ever to access information on handling finances, the problem persists. Companies like NerdWallet make it easier to evaluate options for things like credit cards and student loans, but there are 2 primary issues as I see it:

On the second point – everyone has their own unique situation and unless you have hours upon hours to spend sifting through the web, it’s very hard to find personalized advice. From my experience as an Australian working in New York, the best advice I’ve received has either come from professional experts (like accountants) who are very expensive, or other Aussies in the same boat as I am. That’s where a company like Summer comes into play. Summer is a public benefit corporation that is on a mission to act as a “trusted advisor” to student loan borrowers. From Summer Co-Founder, Will Sealy, “we’re trying to create the software that democratizes [student loan] expertise, that gets the expertise into the hands of the end consumer, who might not be able to afford an accountant”. Basically, students enter information about their personal finances, Summer evaluates thousands of financing options and then recommends the best path forward. They’re solving the problem of not having personalized information. The best part is that this service is free to students – instead, Summer sells through enterprises and other organizations that can offer the product as a benefit to employees. A positive-sum solution. There are other startups in this space, like Mos, which helps students get every dollar of financial aid they qualify for, by simplifying the process of applying to government aid and scholarships. Another startup, Pillar, helps students understand and pay off their debt. Their app connects with a student loan servicer and bank, and then makes personalized suggestions based on loan amount, income, and spending. As the app finds ways for students to make a dent in their overall debt, it will send alerts with the proper advice. The overall takeaway is that whilst these startups are not laying a new foundation for how student loans are issued, they are using the power of data to provide individuals with personalized advice, by looking at thousands of options and presenting the best ones. In this sense, they are like NerdWallet 2.0 in that they don’t just present information, but they actually use your inputs to offer tailored outputs. And, for the most part, they only get paid if you save money i.e. they only capture a percentage of the value they create. Conclusion Student loans – and ISAs in particular – are deeply complex. Whilst there is no doubt that structural change is required in the student loan market, it remains to be seen what the most effective solutions will be. Some closing thoughts:

Finally, I would be remiss if I didn’t mention this – the student loan market is extremely complex. This article might feel like a stream of consciousness and that’s because there’s simply too much to cover, and so much that I am yet to understand. Any mistakes, oversights, counter-arguments, or questions – please feel free to reach out to me. You can contact me via email or Twitter. Comments are closed.

|